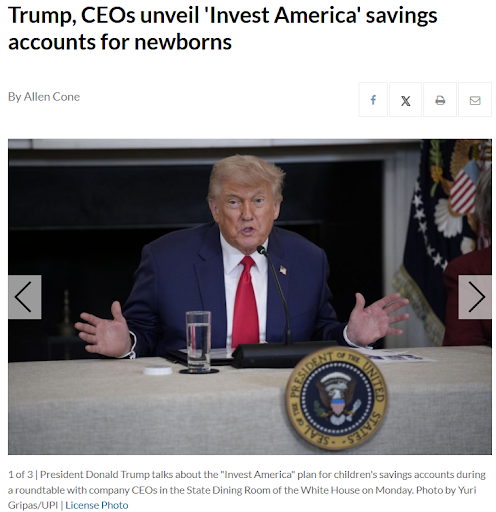

On Monday, President Trump assembled a roundtable of US CEOs to tout his new 401k-like savings program for newborn children, that’s part of the “Big Beautiful Bill.”

A tax-advantaged investment account of $1,000 would be created for every newborn baby with a Social Security number. That money would be invested in the S&P 500 and families and employers could supplement it with up to $5,000 annually.

Dell Technologies CEO, Michael Dell, told the roundtable he would pledge a $1,000 match for any “Trump Account” set up for the new children of his employees.

Other CEOs who promised to support the plan once it passed included Uber’s Dara Khosrowshani, Goldman Sachs’ David Solomon, and Vladimir Tenev of Robinhood.

Brad Gerstner, the CEO of Altimeter Capital who endorsed the concept years ago, briefed attendees on how the plan would seed index fund accounts with $1,000 in government money for each of the 3.7 million US newborns each year:

“Using the power of compound interest. We can eventually make everyone an owner in America. Think of 401(k)s from birth, where corporations will then match those grants to those kids at birth, where parents now who were afraid or didn’t know how to open up an account can now save 50 bucks a week or 100 bucks every couple of weeks. After three decades, a 30-year-old today would have over $270,000 in an Invest America account.”

This is a good idea, if the nest egg money is used to offset future welfare benefits. But a MUCH better idea would be to allow all workers under the age of 35 to place 10% of each paycheck into one of these personal accounts in lieu of paying payroll taxes. This would be the biggest tax cut, the biggest debt reduction plan (wiping out tens of trillions of dollars of future federal liabilities), and the biggest pro-growth plan in world history.