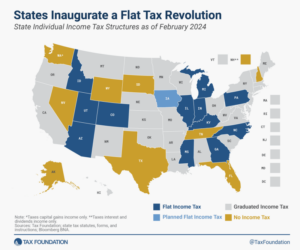

While we are waiting for a new non-income tax state, flat taxes have boomed in recent years.

According to the Tax Foundation:

In the 15 months from July 2021 to September 2022, five states enacted laws to transform their graduated-rate income taxes into single-rate tax structures: Arizona enacted flat tax legislation in July 2021, followed by Iowa in March 2022, Mississippi and Georgia in April 2022, and Idaho in September 2022.