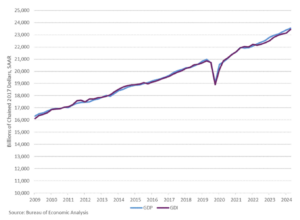

Yesterday’s GDP revisions were very positive. Not only did the headline number improve from 3.0% in the advance estimate to 3.3% but government purchases were simultaneously revised down from growth to contraction, while consumer spending was revised higher. That means private growth was above the headline number.

Best of all was the surge in real gross domestic income, which rose 4.8% last quarter. The average growth rate of real GDP and real GDI was a healthy 4.0%. Low inflation raised real growth.

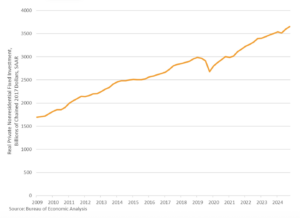

Real private nonresidential fixed investment–the driver of long-run economic growth–was also revised higher to 5.7% and that’s on top of a 10.3% increase in the first quarter. The decline in overall investment was due to nonfarm inventories being sold off, after those inventories were imported in the first quarter to front run tariffs.

Caution: The latest GDP NOW forecast for quarter 3 growth is 2.2%, and we think tariffs are the biggest pullback on maintaining 3%+ growth.